Buy Now, Pay Later

- – 4-month term

- – No impact on credit to apply

- – Instant approval decision

- – Secure and straightforward checkout

Ready to go? Add this product to your cart and select a plan during checkout.

Payment plans are offered through our trusted finance partners Klarna, Affirm, Afterpay, Apple Pay, and PayTomorrow. No-credit-needed leasing options through Acima may also be available at checkout.

Learn more about financing & leasing here.

This item is eligible for return within 30 days of receipt

To qualify for a full refund, items must be returned in their original, unused condition. If an item is returned in a used, damaged, or materially different state, you may be granted a partial refund.

To initiate a return, please visit our Returns Center.

View our full returns policy here.

Description

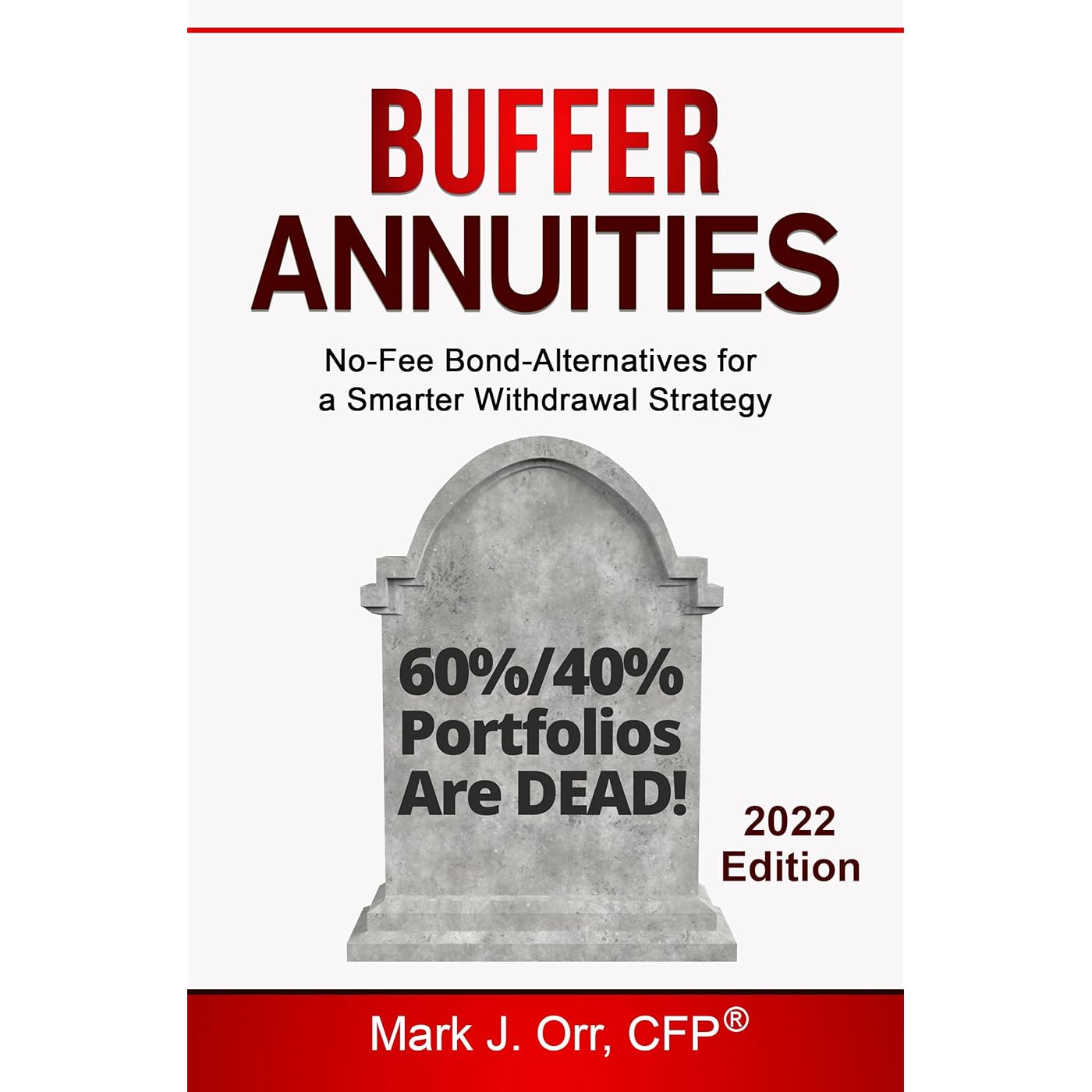

There are only two doors to retirement. You either outlive your money… or your money outlives you. There is NO THIRD DOOR! Do you ever worry about living longer than your money? How about the interest rates you’re getting on your bonds compared to inflation nowadays? Even the value of bonds has been dropping over the last year or so. So much for so-called “safe” bonds. Do you also worry about the big swings your stocks and mutual funds endure? The Problem: During 2019 and 2020, JP Morgan, Bank of America, and Barron’s declared that the 60/40 portfolio should NOT be relied upon. The traditional 60/40 portfolio (60% stocks and 40% bonds) and the “4% Rule” can no longer be counted on for not outliving your money in retirement. You will learn precisely why the author and so many others believe this in this book – and how that can adversely affect your future. In 2022 and beyond, retirees will need better income withdrawal and Required Minimum Distribution (RMD) strategies to survive and thrive in a 25-30+ year retirement. Potential Solution: It was on Wednesday, February 3rd, 2021, when it all came together in my mind. A marriage of sorts. A relatively new type of accumulation annuity married with a smarter withdrawal strategy to outdo the “4% rule” or a typical 60%/40% portfolio. Within days, I was outlining this book to share my breakthrough strategy. The withdrawal strategy uses what I call “BUFFER ANNUITIES” that can radically improve the probability of retirement success of both the 60/40 portfolio and the suspect 4% rule. BUFFER ANNUITIES are my code name for a little-known tiny subset of fixed annuities and are a vital ingredient of this simple yet highly effective IRA withdrawal strategy. These BUFFERS are a near-perfect bond alternative. Portfolio 60/40 Headwinds: The 40-year bull market for bonds is apparently over (due to rising interest rates), and stocks are near historically high valuations - according to many on Wall Street. That includes mutual fund giant Vanguard. You’ll see their stock and bond market predictions for the next decade inside my book too. They send it only to financial advisors. Hint: Vanguard says that the returns over the next decade will not be NEARLY AS GOOD as the last. Warren Buffet said this about bonds in 2021: "Bonds are not the place to be these days," the legendary investor wrote in Berkshire Hathaway's annual letter to shareholders, lamenting that the yield on 10-year Treasury bonds has fallen 94% since September 1981. Dr. Wade Pfau, CFA, told Forbes in 2015: “bonds don’t belong in a retirement portfolio.” And that was when interest rates were higher than today! So, what is Wall Street’s current collective advice for retirees? Buy more stocks instead of bonds. A 70/30 or an 80/20 portfolio? But most retirees do not want more stock market risk. They don’t want a repeat of 2008. If bonds are not the safe haven they are supposed to be, what do you do? If you, too, are wary of bonds with meager current interest rates, BUFFERS can easily provide 5%, 6%, 7%, or much higher average returns – with none of the risks inherent with bonds (credit risk, interest rate risk, inflation risk). Hate paying fees for bond mutual funds or ETFs or to a financial advisor? If so, BUFFERS have no mandatory fees or expenses. Zero costs. But most importantly, if you are looking for an almost fool-proof, 3-step income withdrawal or RMD system, this book is a must-read. The bottom line. This book teaches a proven, common-sense withdrawal strategy for improving the likelihood that you will never run out of retirement money. And do so without the risks and fees associated with bond funds and bond ETFs. FULLY UPDATED for 2022! [FIA, index annuities, RMD, withdrawal strategies, bond alternatives] Read more

Publication date : August 12, 2021

Language : English

File size : 4178 KB

Text-to-Speech : Enabled

Screen Reader : Supported

Enhanced typesetting : Enabled

X-Ray : Not Enabled

Word Wise : Enabled

Print length : 101 pages

Frequently asked questions

To initiate a return, please visit our Returns Center.

View our full returns policy here.

- Klarna Financing

- Affirm Pay in 4

- Affirm Financing

- Afterpay Financing

- PayTomorrow Financing

- Financing through Apple Pay

Learn more about financing & leasing here.